Ahead of the Game: Understanding Fraud Risk Assessment as a Preventive Technique in Forensics

The adage “an ounce of prevention is worth a pound of cure” rings true when it comes to fraud. By proactively identifying and addressing potential fraud risks, organisations can avoid the costly and time-consuming reactive processes of investigations. That's where Fraud Risk Assessment comes in!

Forensic accountants are increasingly turning to preventive techniques like FRA to help clients stay ahead of the game.

Forensic accounting is a specialised field of accounting that involves the application of accounting, auditing, and investigative skills to detect and prevent fraud. It plays a critical role in identifying financial irregularities and providing evidence that can be used in legal proceedings.

Fraud Risk Assessment (FRA) is a key component of forensic accounting. It involves the identification, analysis, and evaluation of potential fraud risks to an organisation. By conducting a thorough FRA, organisations can take proactive steps to prevent fraud before it occurs.

By the end of this article, you will have a better understanding of FRA as a preventive forensic activity and its importance in detecting and preventing fraud.

Uncovering the Roots of Risk: Exploring the Genesis and Assessment of Potential Threats

In today's business world, risks are an inherent part of any organisation's operations. Understanding the concept of risk and its relevance in business is essential to manage them effectively. Risk can be defined as the possibility of an event occurring that will have a negative impact on an organisation's ability to achieve its objectives. There are various types of risks faced by businesses, including financial, operational, strategic, and reputational risks.

Identifying, analysing, and evaluating risks is a critical component of risk management. The process starts with identifying risks that may impact the organisation's objectives. Risk analysis involves assessing the probability and impact of risks on the organisation. Finally, risk evaluation compares the results of the risk analysis with pre-determined risk criteria to determine the significance of the risk.

The Power of Fraud Risk Assessment: A Proactive Approach to Combatting Fraud

In the context of fraud prevention, the role of risk assessment is critical. Fraud Risk Assessment (FRA) is the process of identifying and evaluating the risks of fraud within an organisation. The purpose of FRA is to identify potential fraud risks and develop strategies to mitigate them. By conducting FRA, organisations can proactively identify potential fraud risks, implement control measures, and prevent fraudulent activities from occurring. FRA can help organisations achieve their objectives by reducing the risk of fraud and increasing operational efficiency.

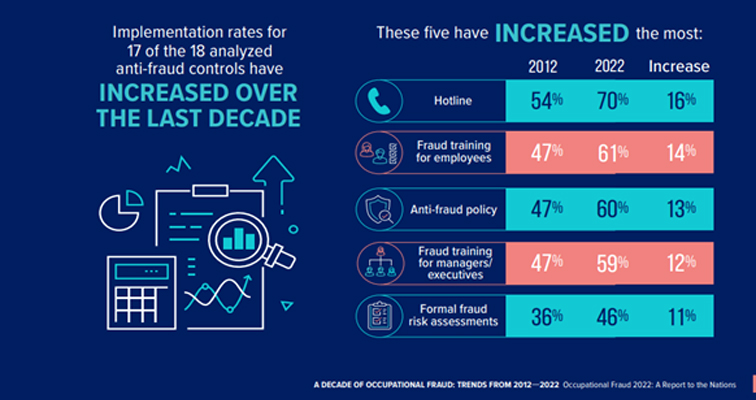

In its 2022 Report to Nations, the ACFE notes that formal fraud risk assessments have seen an increase in implementation rates for anti-fraud policies over the past decade.

The benefits of conducting FRA include: -

- Reducing the likelihood of fraud occurring,

- Minimising the potential financial impact of fraud on the organisation,

- Enhancing the overall effectiveness of the organisation's control environment, and

- Demonstrating a commitment to ethical business practices.

While internal audit focuses on evaluating and improving internal control systems and compliance with policies and regulations, FRA focuses specifically on identifying potential fraud risks and developing strategies to prevent and detect fraud. FRA goes beyond traditional audit procedures and requires specialised knowledge and expertise in forensic accounting.

Striking the Right Balance: Identifying the Sweet Spot of Business

Before getting into “assessing” fraud risk, identifying the risk appetite of an organisation is important. Identifying the "sweet spot of business" refers to the optimal balance between risk-seeking and risk avoidance that can help a company achieve its objectives while managing potential risks. Just like in baseball, where the "sweet spot" is the point on a bat where maximum energy can be transferred to the ball, businesses need to find the right equilibrium between risk and reward. Too much risk-taking can lead to speculative endeavours and business failure, while excessive risk aversion can cause organisations to miss out on market opportunities and fall behind emerging trends. Forensic accountants and other risk management professionals play a pivotal role in helping companies strike the right balance between risk and reward. They need to identify, analyse, and evaluate the various types of risks that a company may face and determine the optimal level of risk that the company should take on.

The level of risk can be classified into three categories, inadequate risk-taking, optimal risk-taking, and excessive risk-taking. It is essential to find the right balance because taking too little risk may lead to missed opportunities while taking too much risk can result in severe losses. FRA plays a crucial role in identifying and managing risks to achieve the sweet spot of business. By conducting an FRA, companies can identify potential risks and implement measures to mitigate them, ensuring they are taking optimal risks and maximising their expected value.

Stages and Techniques in Fraud Risk Assessment

FRA involves several stages and techniques to identify and evaluate the risks faced by a company. The planning stage ensures compliance with professional standards and regulatory stipulations, and risks are identified as inherent and residual. The inherent risk is affected by various factors, such as the business environment, the effectiveness of internal controls, and the ethics and values of the company. To gather information and assess potential risks, FRA uses various techniques such as anonymous feedback, surveys, focus groups, structured questionnaires, technical discussions with experts, and brainstorming with technical and domain experts.

However, selecting the right technique for conducting FRA is crucial for its effectiveness. The technique should be appropriate for the nature and circumstance of the company and the type of risk being assessed. An unsuitable technique can result in inaccurate or incomplete results, leading to inadequate identification and management of fraud risks. Therefore, selecting the right technique can help in obtaining the necessary information to identify and evaluate risks, as well as potential control measures to mitigate such risks. A comprehensive and effective FRA process can proactively detect and prevent fraud and minimise the associated financial and reputational damages.

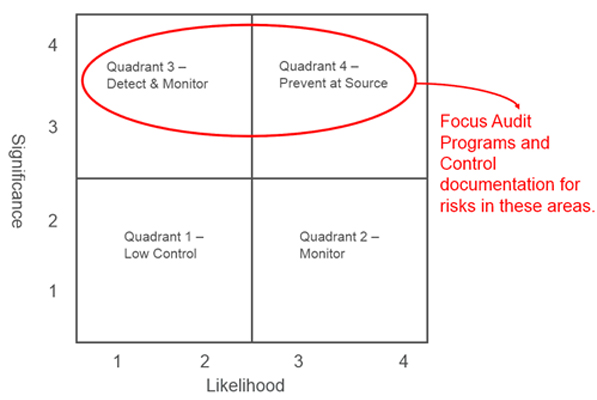

Importance of Risk Quadrants in Fraud Risk Assessment

In the process of FRA, once the potential risks have been identified and assessed, the concept of risk quadrants can be utilised to evaluate further and prioritise them. The risk quadrants are an essential tool for organisations to determine the likelihood and impact of potential risks. By placing each risk in its respective quadrant, an organisation can assess which risks require immediate attention and which can be monitored over time.

The process involves identifying potential risks, analysing their likelihood of occurrence, and evaluating their potential impact. Prioritising risks through this process helps organisations to develop a risk management plan to mitigate or avoid them. The concept of risk quadrants further aids in prioritising risks and enables organisations to focus their resources on the risks that require immediate attention. With a comprehensive approach to FRA, organisations can prevent and detect fraudulent activities, ensuring a safe and sustainable business environment.

Following is an example: -

Mitigating Control and Remediation of Risk

Mitigating controls and remediation of risk are integral parts of a comprehensive fraud risk management program. Mitigating controls are evaluated based on their adequacy of design and operation effectiveness, which help determine their effectiveness in mitigating fraud risks. By identifying the extent to which they can rely on controls, organisations can develop effective strategies to identify, assess, and mitigate fraud risk.

However, despite implementing controls, there might still be residual risks. The remediation of risk process addresses these risks by developing plans to reduce residual risk to an acceptable level. The process owners develop a remediation plan, and the internal audit tracks and reports the management's progress towards its implementation. The remediation process is crucial in protecting organisations against potential fraud threats and plays a vital role in the overall risk management process. In essence, mitigating controls help prevent fraud and minimise risk impact, while remediation of risk ensures that residual risks are reduced to an acceptable level.

Integrating Fraud Risk Assessment

Integrating the results of the assessment (FRA) into the annual risk assessment and audit planning is a critical step in ensuring that significant financial, operational, and information system risks are appropriately addressed. The FRA identifies potential fraud risks that could impact the organisation, which is then integrated with the annual risk assessment. This helps prioritise audits based on their relative level of risk, which includes multiple risk factors in addition to fraud risk.

By prioritising audits based on risk, organisations can allocate resources effectively, minimise the impact of risks on their operations, and improve overall risk management. This helps organisations identify and address critical risks in a timely and effective manner, reducing the potential for financial losses and reputational damage.

Moreover, integrating FRA into the annual risk assessment ensures that fraud risks are not considered in isolation but are evaluated along with other operational and financial risks. This helps create a more comprehensive risk management program that considers all potential risks faced by the organisation. A comprehensive risk management program that addresses all potential risks faced by the organisation is crucial to protect against financial losses and reputational damage.

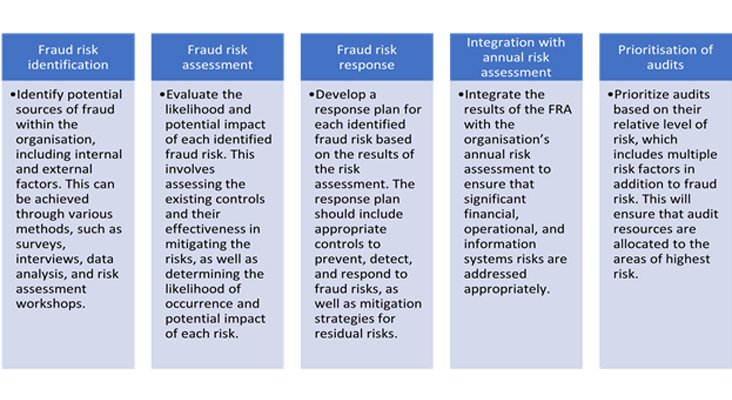

Suggested Framework for Fraud Risk Assessment:

By following a structured approach to FRA, organisations can identify and mitigate fraud risks in a proactive manner, reducing the potential impact of fraud on the organisation.

In conclusion, Fraud Risk Assessment is an important tool for forensic accountants to prevent fraud before it occurs. By conducting a comprehensive FRA, forensic professionals can help their clients identify potential fraud risks, evaluate their likelihood and impact, and develop an effective response plan to mitigate or avoid them. Forensic accountants can offer this service to their clients as a proactive measure to protect their financial well-being and reputation. With the ever-increasing threat of fraud, organisations cannot afford to ignore the importance of FRA in their risk management program.